Maximizing Charitable Donations Under the New Tax Law

Many people will no longer be able to itemize under the new Tax Cuts and Jobs Act, which means that charitable donations won't be as valuable from a tax perspective. Here are some ways to maximize your charitable giving and still receive some tax benefit: 1. Accelerate your 2018 donations into...

Summary of the New Tax Law – The Tax Cuts and Jobs Act of 2017

The Tax Cut and Jobs Act of 2017 was passed by Congress earlier this week and signed by President Trump this morning. Since 2017 is winding up, I wanted to pass along a quick summary of the tax bill. If you are one of the many Americans who will no longer be itemizing under the new bill, you may...

The Equifax Data Breach and Keeping Your Info Safe

By now, most of you have heard about the Equifax data breach. It is estimated that 143 million Americans were affected by this data breach so even if you weren't affected, chances are you know someone who was. Equifax has a tool on their website that allows you to check and see if your data was...

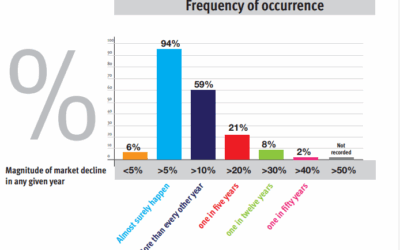

The Right Things to do in a Volatile Market

"Don't panic." "Don't sell at the bottom." "Don't try to time the market." You're used to being told what you shouldn't do when the market is falling. Today I'd like to talk about the right things to do in a volatile market. The Market is Cyclical: Expect ups and downs Before we discuss the...

Congress Extends Tax Breaks for 2015 and Beyond

In what has become an annual ritual, Congress recently passed a last minute bill to extend tax laws that expired at the end of 2014. The good news is that some of these extenders are now permanent, which will eliminate the need to extend them in future years. Other provisions were extended just...

Budget Deal Eliminates Important Social Security Filing Strategies

Earlier this week President Obama signed the 2016 budget deal which included several surprise provisions for Social Security. The two biggest changes will be to the “file and suspend” strategy and the ability to file a “restricted application”. The loss of these two strategies will affect many...